As filed with the Securities and Exchange Commission on January 3, 2024

Registration No. 333-273841

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 3 TO FORM F-1

REGISTRATION STATEMENT UNDER

THE SECURITIES ACT OF 1933

GENIUS GROUP LIMITED

(Exact name of Registrant as specified in its charter)

Not Applicable

(Translation of Registrant’s name into English)

| Singapore | 8200 | Not Applicable | ||

(State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification number) |

8 Amoy Street, #01-01

Singapore 049950

Tel: +65 8940 1200

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

Puglisi & Associates

850 Library Avenue, Suite 204

Newark, DE 19711

Tel: (302) 738-6680

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies of all communications, including communications

sent to agent for service, should be sent to:

Jolie Kahn, Esq. 12 E. 49th Street, 11th floor New York, NY 10017 Tel: (516) 217-6379 Fax: (866) 705-3071 |

Katten Muchin Rosenman LLP 525 W. Monroe Street Chicago, IL 60661-3693 Attn: Mark D. Wood Alyse Sagalchik Tel: (312) 902-5200 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933.

| Emerging growth company | ||

| ☒ |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any jurisdiction where the offer or sale is not permitted.

| PRELIMINARY PROSPECTUS | SUBJECT TO COMPLETION | DATED JANUARY 3, 2024 |

Series 1 Units, each consisting of One Ordinary Share

and One Series 2024 -A Warrant to Purchase One Ordinary Share and One Series 2024-C Warrant to Purchase One Ordinary Share

and

Series 2 Units, each consisting of One Pre-Funded Series 2024 -B Warrant to Purchase

One Ordinary Share and One Series 2024 -A Warrant

to Purchase One Ordinary Share and One Series 2024-C Warrant to Purchase One Ordinary Share

Genius Group Limited

We are offering for sale up to 15,673,981 Series 1 units (at an assumed offering price of $0.7018 per unit, which was the closing price of an ordinary share of the Company on December 27, 2023, which is assumed for purposes of calculations in this preliminary prospectus and is subject to final pricing upon effectiveness, and to be known as the “assumed offering price”), with each Series 1 unit consisting of one ordinary share and one Series 2024 -A warrant to purchase one ordinary share and one Series 2024-C warrant to purchase one ordinary share. Each full Series 2024 -A warrant entitles the holder thereof to purchase one ordinary share. Each full Series 2024-C warrant entitles the holder thereof to purchase one ordinary share. Each Series 1 unit will be sold at a fixed price of $0.7018 (at the assumed offering price) per Series 1 unit until the completion of this offering. The Series 1 units will not be issued or certificated. The ordinary shares and the Series 2024 -A warrants and Series 2024-C warrants are immediately separable and will be issued separately but will be purchased together in this offering.

We are also offering to those purchasers, whose purchase of Series 1 units in this offering would otherwise result in the purchaser, together with its affiliates and certain related parties, beneficially owning more than 4.99% (or, at the election of the purchaser, 9.99%) of our outstanding ordinary shares following the consummation of this offering, the opportunity to purchase, if such purchaser so chooses, to purchase, in lieu of some or all Series 1 units, up to 15,673,981 Series 2 units. Each Series 2 unit will consist of one pre-funded Series 2024 -B warrant to purchase one ordinary share and one Series 2024 -A warrant to purchase one ordinary share and one Series 2024-C warrant to purchase one ordinary share. Each full pre-funded Series 2024 -B warrant entitles the holder thereof to purchase one ordinary share. Each Series 2 unit will be sold at a fixed price of $0.7018 per Series 2 unit minus $0.0001 (which is the per share exercise price of each pre-funded Series 2024-B warrant). For each Series 2 unit we sell, the number of Series 1 units we are offering will be decreased on a one-for-one basis. Because we will issue one Series 2024 -A warrant and one Series 2024-C warrant as part of each Series 1 unit and Series 2 unit, the number of Series 2024 -A warrants and Series 2024-C warrants sold in this offering will not change as a result of a change in the mix of the Series 2 units and Series 1 units sold. The Series 2 units will not be issued or certificated. The pre-funded Series 2024 -B warrants and the Series 2024 -A warrants and Series 2024-C warrants are immediately separable and will be issued separately but will be purchased together in this offering. The ordinary shares issuable from time to time upon exercise of the Series 2024 -A warrants and the Series 2024-C warrants and the pre-funded Series 2024 -B warrants are also being offered pursuant to this prospectus.

The Series 2024 -A warrants, with an assumed exercise price of $0.7018 per ordinary share, will be exercisable commencing on the date of issuance and will expire on the five-year anniversary of the date of issuance. The Series 2024-C warrants, with an assumed exercise price of $0.7018 per ordinary share, will be exercisable commencing on the date of issuance and will expire on the 18-month anniversary of the date of issuance. The pre-funded Series 2024 -B warrants will be exercisable commencing on the date of issuance and will expire on the five-year anniversary of the date of issuance, with an exercise price of $0.0001 per ordinary share. The assumed purchase price of $0.7018 per Series 2 unit will be pre-paid, except for a nominal exercise price of $0.0001 per ordinary share subject to the pre-funded Series 2024-B warrants, upon issuance of the pre-funded Series 2024 -B warrants and, consequently, no additional payment or other consideration (other than the nominal exercise price of $0.0001 per share) will be required to be delivered to us by the holder upon exercise of the pre-funded Series 2024 -B warrants. See “Description of Warrants” for more information on the securities offered hereby.

The placement agent has agreed to use reasonable best efforts to arrange for the sale of the securities. There is no required minimum number of securities or amount of proceeds that must be sold as a condition to completion of this offering.

Our ordinary shares are listed on the NYSE American under the symbol “GNS.” The Series 2024 -A warrants, the Series 2024-C warrants and the pre-funded Series 2024 -B warrants are not, and will not be, listed for trading on any national securities exchange or other trading system.

We are both an “emerging growth company” and a “foreign private issuer” as defined under the U.S. federal securities laws and, as such, may elect to comply with certain reduced public company reporting requirements for this and future filings. See “Prospectus Summary — Implications of Being an Emerging Growth Company” and “Prospectus Summary — Implications of Being a Foreign Private Issuer.”

Investing in our ordinary shares involves a high degree of risk. See “Risk Factors” beginning on page S-14. Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

We have retained H.C. Wainwright & Co., LLC, or the placement agent, as our exclusive placement agent to use its reasonable best efforts to solicit offers to purchase the securities in this offering. The placement agent has no obligation to buy any of the securities from us or to arrange for the purchase or sale of any specific number or dollar amount of the securities. We have agreed to pay the placement agent fees set forth in the table below, which assumes that we sell all of the securities we are offering. There is no arrangement for funds to be received in escrow, trust or similar arrangement. There is no minimum offering requirement as a condition of closing of this offering. We will bear all costs associate with the offering. See “Plan of Distribution” for more information regarding these arrangements.

| Per Series 1 Unit | Per Series 2 Unit | Total | ||||||||||

| Public offering price | $ | $ | $ | |||||||||

| Placement agent fees(1) | $ | $ | $ | |||||||||

| Proceeds, before expenses, to us(2) | $ | $ | $ | |||||||||

| (1) | We have also agreed to reimburse the placement agent’s legal fees and expenses in the amount of up to $150,000. See “Plan of Distribution” for a description of the compensation to be received by the placement agent. | |

| (2) | Because there is no minimum offering amount required as a condition to closing in this offering, the actual public offering amount, placement agent fees and proceeds to us, if any, are not presently determinable and may be substantially less than the total maximum offering amounts set forth above. For more information, see “Plan of Distribution.” |

Delivery of the ordinary shares, the Series 2024 -A warrants and the Series 2024-C warrants and the pre-funded Series 2024 -B warrants, if any, offered hereby is expected to be made on or about ________, 2024.

H.C. WAINWRIGHT & CO.

The date of this prospectus is __________, 2024.

Table Of Contents

| i |

About This Prospectus

Except where indicated or where the context otherwise requires, the terms “Genius Group,” “we,” “us,” “our,” the “Company,” “our Company”, “company” and “our business” refer to Genius Group Limited together with its consolidated subsidiaries. For explanations of certain other terms used in this prospectus, please read “Prospectus Summary — Overview — A Brief Glossary” beginning on page S-3.

You should rely only on the information contained in this prospectus. We have not, and the placement agent has not, authorized anyone to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. We are not, and the placement agent is not, making an offer to sell securities in any jurisdiction where the offer or sale is not permitted. You should not assume that the information contained in this prospectus is accurate as of any date other than the date on the front of this prospectus.

For investors outside of the United States of America (the “United States” or the “U.S.”): Neither we nor the placement agent has done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction, other than the United States, where action for that purpose is required. Persons outside of the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of our ordinary shares and the distribution of this prospectus outside of the United States.

The Company’s reporting currency is the U.S. dollar. The functional currencies of the Genius Group and its subsidiaries are their local currencies (Singapore dollar, British pound, Indonesian rupiah and South African Rand, New Zealand Dollar) and the functional currency of ERL, UAV and RF is the U.S. dollar. The Company engages in foreign currency denominated transactions with customers and suppliers, as well as between subsidiaries with different functional currencies. Gains and losses resulting from transactions denominated in non-functional currencies are recognized in earnings.

.

Unless otherwise noted, (i) all industry and market data in this prospectus is presented in U.S. dollars, (ii) all financial and other data related to Genius Group in this prospectus is presented in U.S. dollars, (iii) all references to “$” or “USD” in this prospectus (other than in our financial statements) refer to U.S. dollars, and (iv) all references to “S$” or “SGD” in this prospectus refer to Singapore dollars.

Our fiscal year end is December 31. References to a particular “fiscal year” are to our fiscal year ended December 31 of that calendar year. Our audited consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (“IFRS”), as issued by the International Accounting Standards Board.

We obtained the industry, market and competitive position data in this prospectus from our own internal estimates, surveys, and research as well as from publicly available information, industry and general publications and research, surveys and studies conducted by third parties. None of the independent industry publications used in this prospectus were prepared on our behalf. Industry publications, research, surveys, studies and forecasts generally state that the information they contain has been obtained from sources believed to be reliable, but that the accuracy and completeness of such information is not guaranteed. Forecasts and other forward-looking information obtained from these sources are subject to the same qualifications and uncertainties as the other forward-looking statements in this prospectus, and to risks due to a variety of factors, including those described under “Risk Factors.” These and other factors could cause results to differ materially from those expressed in these forecasts and other forward-looking information.

Unless we indicate otherwise or the context otherwise requires, all information in this prospectus gives effect to the 6-for-1 share split with respect to our ordinary shares, which took effect on April 29, 2021.

We have proprietary rights to trademarks used in this prospectus that are important to our business, many of which are registered under applicable intellectual property laws. Solely for convenience, the trademarks, service marks and trade names referred to in this prospectus are without the ®, ™ and other similar symbols, but the absence of such references is not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the rights of the applicable licensors to these trademarks, service marks and trade names.

| S-1 |

This prospectus contains additional trademarks, service marks and trade names of others. All trademarks, service marks and trade names appearing in this prospectus are, to our knowledge, the property of their respective owners. We do not intend our use or display of other companies’ trademarks, service marks or trade names to imply a relationship with, or endorsement or sponsorship of us by, any other person.

This prospectus has not been registered as a prospectus with the Monetary Authority of Singapore. Accordingly, our ordinary shares were not offered or sold or caused to be made the subject of an invitation for subscription or purchase and will not be offered or sold or caused to be made the subject of an invitation for subscription or purchase, and this prospectus or any other document or material in connection with the offer or sale, or invitation for subscription or purchase, of our ordinary shares, has not been circulated or distributed, nor will it be circulated or distributed, whether directly or indirectly, to any person in Singapore other than (i) to an institutional investor (as defined in Section 4A of the Securities and Futures Act 2001 of Singapore, as modified or amended from time to time (“SFA”)) pursuant to Section 274 of the SFA, (ii) to a relevant person (as defined in Section 275(2) of the SFA) pursuant to Section 275(1) of the SFA, or any person pursuant to Section 275(1A) of the SFA, and in accordance with the conditions specified in Section 275 of the SFA and (where applicable) Regulation 3 of the Securities and Futures (Classes of Investors) Regulations 2018, or (iii) otherwise pursuant to, and in accordance with the conditions of, any other applicable provision of the SFA.

Where our ordinary shares are subscribed or purchased under Section 275 of the SFA by a relevant person which is:

(a) a corporation (which is not an accredited investor (as defined in Section 4A of the SFA)) the sole business of which is to hold investments and the entire share capital of which is owned by one or more individuals, each of whom is an accredited investor; or

(b) a trust (where the trustee is not an accredited investor) whose sole purpose is to hold investments and each beneficiary of the trust is an individual who is an accredited investor, securities or securities-based derivatives contracts (each term as defined in Section 2(1) of the SFA) of that corporation or the beneficiaries’ rights and interest (howsoever described) in that trust shall not be transferred within six months after that corporation or that trust has acquired the ordinary shares pursuant to an offer made under Section 275 of the SFA, except:

| ➢ | to an institutional investor or to a relevant person, or to any person arising from an offer referred to in Section 275(1A) of the SFA or Section 276(4)I(ii) of the SFA; | |

| ➢ | where no consideration is or will be given for the transfer; | |

| ➢ | where the transfer is by operation of law; | |

| ➢ | as specified in Section 276(7) of the SFA; or | |

| ➢ | as specified in Regulation 37A of the Securities and Futures (Offers of Investments) (Securities and Securities-based Derivatives Contracts) Regulations 2018. |

Any reference to the SFA is a reference to the Securities and Futures Act 2001 of Singapore and a reference to any term as defined in the SFA or any provision in the SFA is a reference to that term as modified or amended from time to time including by such of its subsidiary legislation as may be applicable at the relevant time.

Notification under Section 309B(1)(c) of the SFA: The Company has determined, and hereby notifies all persons (including relevant persons (as defined in Section 309A(1) of the SFA)) that the ordinary shares are prescribed capital markets products (as defined in the Securities and Futures (Capital Markets Products) Regulations 2018) and Excluded Investment Products (as defined in MAS Notice SFA 04-N12: Notice on the Sale of Investment Products and MAS Notice FAA-N16: Notice on Recommendations on Investment Products).

By accepting this prospectus, the recipient hereof and thereof represents and warrants that such recipient is entitled to receive it in accordance with the restrictions set forth above and agrees to be bound by the limitations contained herein. Any failure to comply with these limitations may constitute a violation of law.

| S-2 |

PROSPECTUS SUMMARY

This summary highlights certain information contained elsewhere in this prospectus. You should read the entire prospectus carefully, including our financial statements and related notes and the risks described under “Risk Factors.” Our actual results and future events may differ significantly based upon a number of factors. The reader should not put undue reliance on the forward-looking statements in this document, which speak only as of the date on the cover of this prospectus.

Overview

A Brief Glossary

To aid in the understanding the entities, acquisitions, products, services and certain other concepts referred to in this prospectus, the following non-exhaustive glossary of terms is provided:

AI is an abbreviation of Artificial Intelligence and refers to technology that enables machine learning, specifically in the case of Genius Group where our Genie virtual assistant is able to recommend personalized steps for each student based on Genie learning the personal strengths, passions, purpose, preferences and level of each student through their inputs on our Edtech platform.

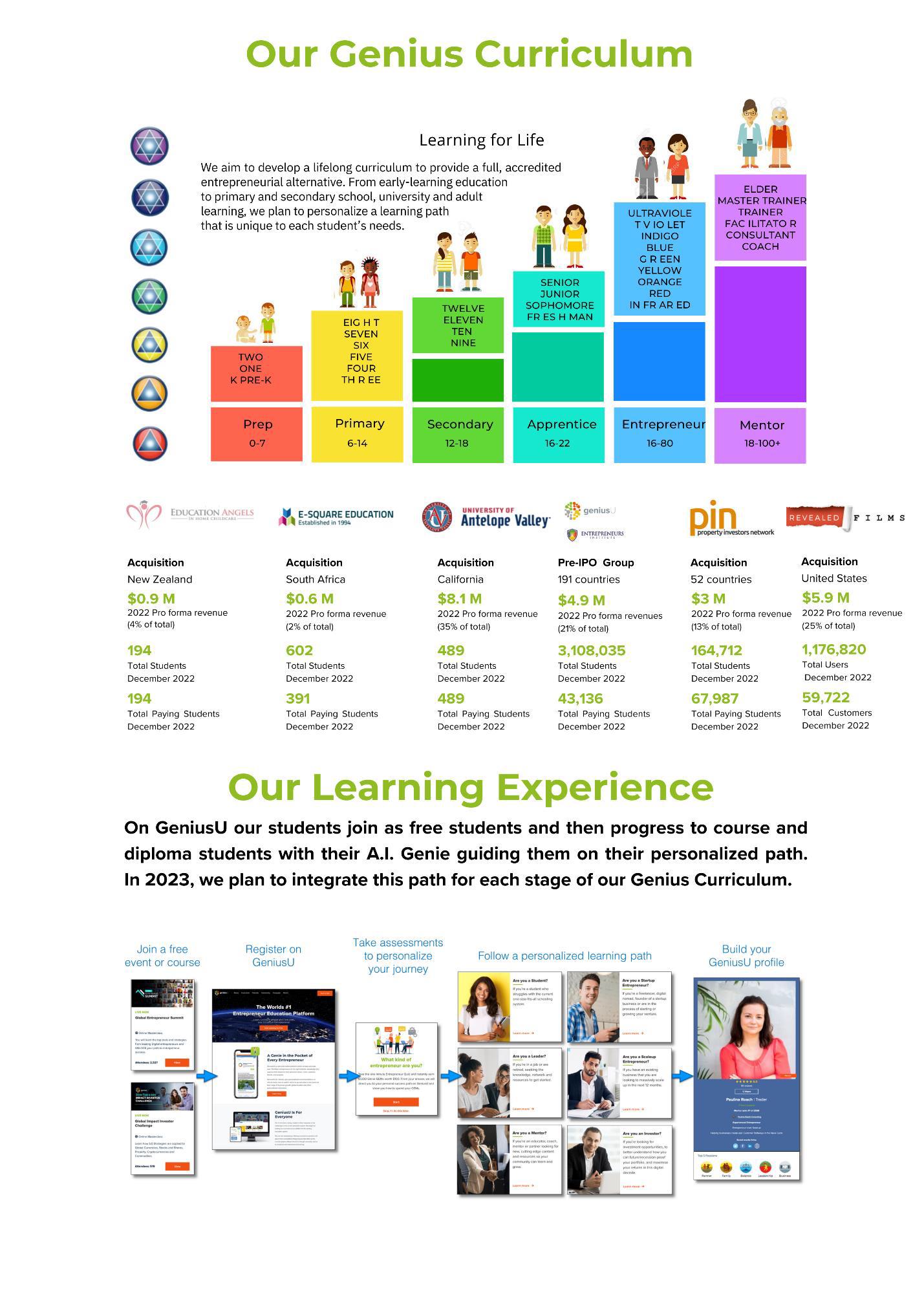

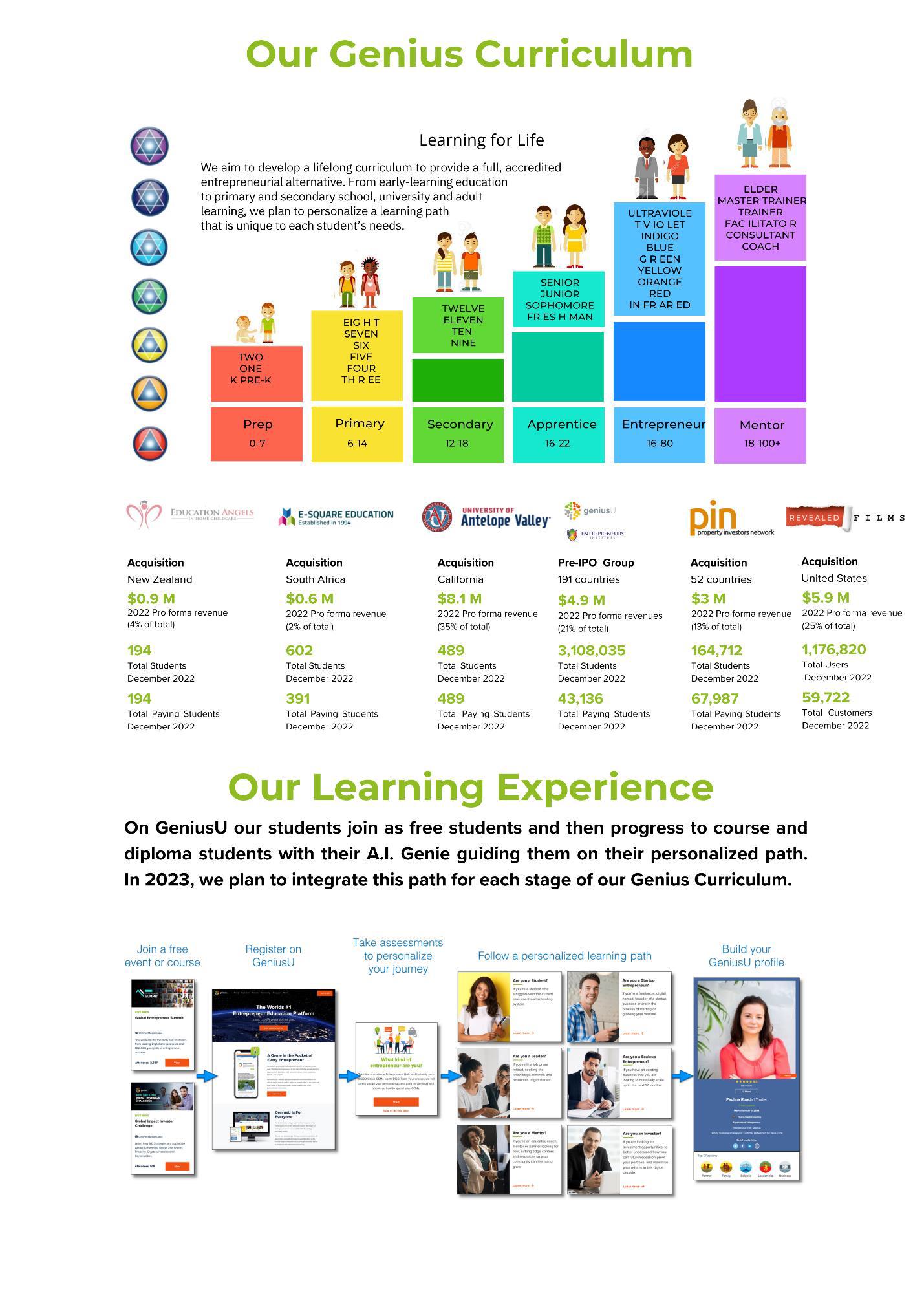

Acquisitions refers to the five companies that we acquired following our IPO including Revealed Films acquired in Oct 2022. The acquisition companies are Education Angels, E-Square, Property Investors Network, University of Antelope Valley and Revealed Films.

Certification refers to the digital courses on our GeniusU platform that faculty members take in order to be certified to mentor students on GeniusU, and to be able to add their own courses and products to GeniusU.

City Leader refers to our Mentors who host monthly events in their city to support the Students and Mentors in their local area.

E-Square refers to E-Squared Education Enterprises (Pty) Ltd, a South African private limited company and one of the Acquisitions as defined below.

Edtech is an abbreviation of Educational Technology and refers to technology designed to improve the effectiveness, efficiency and experience of the education process. Genius Group is focused on growing as an Edtech group with the ability to scale rapidly and operate globally.

Education Angels refers to Education Angels in Home Childcare Limited, a New Zealand private limited company and one of the Acquisitions as defined below.

Entrepreneurs Institute refers to Wealth Dynamics Pte Ltd, a Singapore private limited company and one of the companies in the Pre-IPO Group.

Entrepreneur Resorts refers to Entrepreneur Resorts Limited, a Seychelles public listed company on the Seychelles Merj Stock Exchange (Ticker: ERL). Entrepreneur Resorts was acquired by Genius Group in 2020 (spin-off completed on October 2, 2023).

Genius Group (or the Group) refers to the entire group of companies within Genius Group, which include the four companies in the Pre-IPO Group and, following the closing of their acquisitions, the five Acquisitions as defined below

Genius Group Ltd refers specifically to the holding company, Genius Group Limited, the Singapore public limited company which owns the other companies in the Group. Prior to a corporate name change in August 2019, it was known as GeniusU Pte Ltd. For the avoidance of doubt, references in this prospectus to Genius Group Ltd with respect to periods prior to its August 2019 name change should be understood as references to the company as operated under its previous name.

GeniusU Ltd refers to the company formed in August 2019 under the corporate name GeniusU Pte Ltd, and subsequently converted to a public company, GeniusU Ltd in May 2021 (as distinct from its parent Genius Group Ltd, the current Group holding company, which until August 2019 used the name GeniusU Pte Ltd).

| S-3 |

GeniusU, when used without any corporate suffix or otherwise not as part of a corporate name, refers to the Edtech platform including website, mobile app, AI system, data and software system under the GeniusU brand.

IASB refers to International Accounting Standards Board.

IFRS refers to International Financial Reporting Standards as issued by IASB.

Mentor refers to our faculty members who have taken and passed Certifications on GeniusU.

microcamp refers to courses that are a combination of digital content on our GeniusU Edtech platform and live in-person courses conducted with our Mentors.

microdegree refers to the digital courses on our GeniusU Edtech platform. These are a combination of video, audio and text-based learning with assessments and exercises that students can take in their own time, on their own or with the guidance of our faculty.

microschool refers to the scheduled, live digital courses on our GeniusU Edtech platform. These are similar in format to microdegrees but differ in that they are conducted live together with other students and the guidance of our faculty, with live interaction, feedback and challenge-based presentations, competitions and awards.

Partners refer to all individuals who are creating, marketing delivering or hosting courses on GeniusU and PIN, and all faculty members delivering courses in all other Group companies.

Pre-IPO Group refers to the four companies which were already operating as a group in 2020 prior to the Acquisitions closed in 2022, namely Genius Group Ltd, GeniusU Ltd, Entrepreneurs Institute and Entrepreneur Resorts.

Property Investors Network (or PIN) refers to Property Investors Network Ltd combined with its sister company Mastermind Principles Limited, a United Kingdom (“U.K.”) private limited company and one of the Acquisitions as defined above.

Revealed Films (or RF) refers to Revealed Films Inc, US Corporation and one of the Acquisitions as defined above.

students refer to all individuals who have registered for courses in our Group companies. This is further divided into Free Students, who have registered for free courses, and Paying Students, who have registered and paid for courses.

University of Antelope Valley (or UAV) refers to University of Antelope Valley, Inc., a California corporation and one of the Acquisitions as defined above.

| S-4 |

Our Company

We believe that we are a world leading entrepreneur Edtech and education group based on student numbers with a student base of 3.34 million on GeniusU at the end of June 2023. Our mission is to disrupt the current education model with a student-centered, lifelong learning curriculum that prepares students with the leadership, entrepreneurial and life skills to succeed in today’s market.

To help achieve our mission, we have completed an IPO on NYSE American, on April 14, 2022 and then dual listed the company on Upstream on April 6, 2023 (although we subsequently found that there was little demand for Upstream and on September 19, 2023, Genius Group. Ltd. publicly announced that it had commenced the process to delist its securities from Upstream, which process was completed on September 29, 2023. The Genius Group will have no further contact with Upstream as a result of this delisting. It will not be involved with or take part in any distribution of or listing of the shares of its spun off subsidiary, Entrepreneur Resorts Ltd (“ERL”) on Upstream or any other exchange, which will be the sole responsibility of ERL. The decision to delist the Company from Upstream is due to complex securities regulations arising from the dual listing on Upstream and NYSE and de minimis use of Upstream by GNS shareholders). We have also raised additional capital through a follow-on private placement of a Convertible Note in September 2022. We grew from a Pre-IPO Group of four companies to a post IPO Group of nine companies, once the five Acquisitions closed.

Starting from October 30, 2023, U.S. individuals will no longer have the authorization to engage in securities trading activities (including buying, selling, or depositing) on the Upstream/MERJ Exchange. All U.S. shareholders will be promptly removed from Upstream and their holdings will be transferred back to the ERL book entry system. Investors will still need to follow the process to claim their ERL shares, but these shares will be exclusively held with ERL through the registrar. Shareholders won’t be able to view their positions on Upstream, as they will no longer be maintained in Upstream accounts. Trading these securities won’t be possible after a 6-month period, and shareholders will remain as such until ERL lists on another market or until the SEC accepts the Upstream/MERJ position of 15A-6.

Our Pre-IPO Group includes our holding company, Genius Group Ltd, our Edtech platform, GeniusU Ltd, and two companies that we acquired: Entrepreneurs Institute in 2019 and Entrepreneur Resorts in 2020 (spin-off completed on October 2, 2023).

The entrepreneur education system of our Pre-IPO Group has been delivered virtually and in-person, in multiple languages, locally and globally mainly via our GeniusU Edtech platform to adults seeking to grow their entrepreneur and leadership skills. Our partners and community are global with an average of 8,900 new students joining our GeniusU platform each week in 2023. Our City Leaders have been conducting our events (physically or virtually) in over 100 cities and over 2,500+ faculty members have been operating their microschools using our online tools.

We are now expanding our education system to age groups beyond our adult audience, to children and young adults. The five Acquisitions are our first step towards this. They include: Education Angels, which provides early learning in New Zealand for children from 0-5 years old; E-Square, which provides primary and secondary school education in South Africa; University of Antelope Valley, which provides vocational certifications and university degrees in California, USA; Property Investors Network, which provides property investment courses and events in England, UK; and Revealed Films, a media production company that specializes in multi-part documentaries.

Our plan is to combine their education programs with our current education programs and Edtech platform as part of one lifelong learning system, and we have selected these acquisitions because they already share aspects of our Genius Curriculum and our focus on entrepreneur education.

The five Acquisitions have added $7.6 million in revenue to the Group in the period ended June 30, 2023, which represents 85% of the $8.9 million pro forma Group revenue during this period, while the Pre-IPO Group generated $1.4 million (excluding ERL). For the year ended December 31, 2022, the five Acquisitions have added $18.6 million in revenue to the Group, which represents 79% of the $23.5 million pro forma Group revenue during this period, while the Pre-IPO Group generated $4.9 million.

In coming years, we plan to continue the growth of our Group through a combination of organic growth of our Edtech platform together with the acquisition of various education companies that we believe provide complementary programs that can be added to our Genius Curriculum. This Prospectus provides details of both our acquisition strategy together with our plans to integrate these Acquisitions together with future acquisitions into our Edtech platform, “entrepreneur education” vision, Genius Curriculum and “freemium” student and partner conversion models.

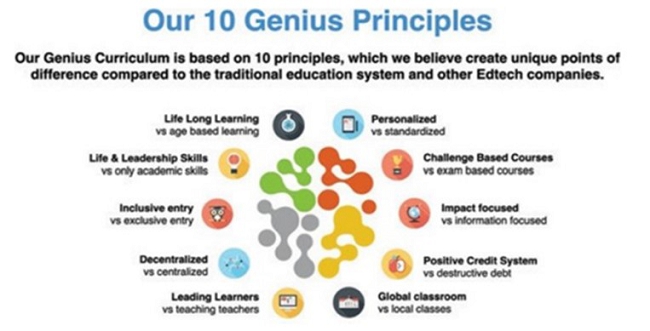

We define “entrepreneur education” as personalized discovery-based learning that leads to higher levels of self-awareness, self-mastery and self-expression. We believe this in turn develops leadership and entrepreneurial skills through which students can independently create value and “create a job” rather than being dependent on a system in which they need to “get a job”. We believe these skills can be nurtured from an early age.

We also believe these skills can be learned at any age, enabling adults to reskill and upskill themselves. We describe our Genius Curriculum, together with the philosophy, principles, learning methodology, course content and delivery of our curriculum in the Business section set forth below in this prospectus.

On December 15, 2023, we publicly disclosed that we have revised our guidance from a net loss of $17 million to a net profit of $3 million as a result to the omission of certain non-cash items.

Roger Hamilton has agreed to convert $1 million of his loan to the Company into Series 1 Units upon the same terms and conditions as offered by this prospectus (the “Founder Securities”). The remaining balance of the loan of approximately $900 thousand shall be repaid in cash at a date no sooner than July 1, 2024.

| S-5 |

Summary of Risks Affecting Our Company

The following is a summary of certain, but not all, of the risks that could adversely affect our business, operations and financial results. If any of the risks actually occur, our business could be materially impaired, the trading price of our ordinary shares could decline, and you could lose all or part of your investment.

Risks Related to Our Business and Industry (All Group companies)

| ➢ | We are a global business subject to complex economic, legal, political, tax, foreign currency and other risks associated with international operations, which risks may be difficult to adequately address. | |

| ➢ | Our growth strategy anticipates that we will create new products, services, and distribution channels and expand existing distribution channels. If we are unable to effectively manage these initiatives, our business, financial condition, results of operations and cash flows would be adversely affected. | |

| ➢ | Our growth may have a negative effect on the successful expansion of our business, on our people management, and on the increase in complexity of our software and platforms. | |

| ➢ | If our growth rate decelerates significantly, our prospects and financial results would be adversely affected, preventing us from achieving profitability. | |

| ➢ | We may be unable to recruit, train and/or retain qualified teachers, mentors, and other skilled professionals. | |

| ➢ | Our business may be materially adversely affected if we are not able to maintain or improve the content of our existing courses or to develop new courses on a timely basis and in a cost-effective manner. | |

| ➢ | Failure to attract and retain students to enroll in our courses and programs, and to maintain tuition levels, may have a material adverse impact on our business and prospects. | |

| ➢ | If student performance falls or parent and student satisfaction declines, a significant number of students may not remain enrolled in our programs, and our business, financial condition and results of operations will be adversely affected. | |

| ➢ | Our curriculum and approach to instruction may not achieve widespread acceptance, which would limit our growth and profitability. | |

| ➢ | The continued development of our brand identity is important to our business. If we are not able to maintain and enhance our brand, our business and operating results may suffer. | |

| ➢ | If our partnerships are unable to maintain educational quality, we may be adversely affected. | |

| ➢ | There is significant competition in the market segments that we serve, and we expect such competition to increase; we may not be able to compete effectively. | |

| ➢ | We cannot assure you that we will not be subject to liability claims for any inaccurate or inappropriate content in our training programs, which could cause us to incur legal costs and damage our reputation. | |

| ➢ | We may be subject to legal liability resulting from the actions of third parties, including independent contractors and teachers, which could cause us to incur substantial costs and damage our reputation. | |

| ➢ | We may not have sufficient insurance to protect ourselves against substantial losses. | |

| ➢ | A cybersecurity attack or other security breach or incident could delay or interrupt service to our users and customers, harm our reputation or subject us to significant liability. |

| S-6 |

Risks Related to Our Business and Industry

| ➢ | We are a growing company with a limited operating history. If we fail to achieve further marketplace acceptance for our products and services, our business, financial condition and results of operations will be adversely affected. | |

| ➢ | Our Edtech platform is technologically complex, and potential defects in our platforms or in updates to our platforms could be difficult or even impossible to fix. | |

| ➢ | System disruptions, capacity constraints and vulnerability from security risks to our online computer networks could impact our ability to generate revenues and damage our reputation, limiting our ability to attract and retain students. | |

| ➢ | Our current success and future growth depend on the continued acceptance of the Internet and the corresponding growth in users seeking educational services on the Internet. | |

| ➢ | We are susceptible to the illegal or improper use of our content, Edtech and platform (whether from students, teachers, mentors, management personnel and other employees, or third parties), or other forms of misconduct, which could expose us to liability and damage our business and brand. |

Risks Related to Our Business and Industry (Specific to Acquisitions)

| ➢ | We have acquired the acquisitions and may pursue other strategic acquisitions or investments. The failure of an acquisition or investment (including but not limited to the Acquisitions) to be completed or to produce the anticipated results, or the inability to fully integrate an acquired company, could harm our business. | |

| ➢ | Public perception and regulatory changes in the primary school and secondary school systems in countries that E-Square may expand to may have a materially adverse impact on the company. | |

| ➢ | Our growth plans for E-Square and our plans to expand into the primary school and high school markets will be a complex and lengthy process where future success is not assured. | |

| ➢ | If we cannot maintain student enrollments and maintain tuition levels in our Acquisition, UAV, the university’s results of operations may be materially adversely affected. |

Risks Related to Investing in a Foreign Private Issuer or a Singapore Company

| ➢ | As a foreign private issuer, we are permitted to follow certain home country corporate governance practices in lieu of certain requirements under the NYSE American listing standards. This may afford less protection to holders of our ordinary shares than U.S. regulations. | |

| ➢ | We are a foreign private issuer and, as a result, we are not subject to U.S. proxy rules and are instead subject to the Securities Exchange Act of 1934, as amended (the “Exchange Act”) reporting obligations that, to some extent, are more lenient and less detailed than those for a U.S. issuer. | |

| ➢ | We may lose our foreign private issuer status, which would then require us to comply with the Exchange Act’s domestic reporting regime and cause us to incur additional legal, accounting and other expenses. |

| S-7 |

6-for-1 Share Split

On April 29, 2021, we effected a 6-for-1 share split with respect to our ordinary shares. Unless we indicate otherwise or the context otherwise requires, all information in this prospectus gives effect to this share split.

Implications of Being an Emerging Growth Company

We qualify as an “emerging growth company” (“EGC”) as defined in the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”). We had less than $1.07 billion in revenue during our last fiscal year, and have not tripped any of the measures that would cause us to no longer qualify as an EGC. As such, we may take advantage of reduced public reporting requirements. These provisions include, but are not limited to:

| ➢ | Being permitted to present only two years of audited financial statements and only two years of related Management’s Discussion and Analysis of Financial Condition and Results of Operations in our filings with the SEC; | |

| ➢ | Not being required to comply with the auditor attestation requirements in the assessment of our internal control over financial reporting; | |

| ➢ | Reduced disclosure obligations regarding executive compensation in periodic reports, proxy statements and registration statements; and | |

| ➢ | Exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and shareholder approval of any golden parachute payments not previously approved. |

We may take advantage of these provisions until the last day of our fiscal year following the fifth anniversary of the date of the first sale of ordinary shares pursuant to the IPO. However, if certain events occur before the end of such five-year period, including if we become a “large accelerated filer,” if our annual gross revenues exceed $1.07 billion or if we issue more than $1.0 billion of non-convertible debt in any three-year period, we will cease to be an emerging growth company before the end of such five-year period.

Section 107 of the JOBS Act provides that an emerging growth company can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act of 1933, as amended (the “Securities Act”), for complying with new or revised accounting standards. We have elected to take advantage of this extended transition period and acknowledge such election is irrevocable pursuant to Section 107 of the JOBS Act.

Implications of Being a Foreign Private Issuer

We report under the Securities Exchange Act of 1934, as amended (the “Exchange Act”), as a non-U.S. company with “foreign private issuer” status. Even after we no longer qualify as an emerging growth company, so long as we qualify as a foreign private issuer under the Exchange Act, we are exempt from certain provisions of the Exchange Act and the rules thereunder that are applicable to U.S. domestic public companies, including:

| ➢ | the rules under the Exchange Act that require U.S. domestic public companies to issue financial statements prepared under U.S. Generally Accepted Accounting Principles (“U.S. GAAP”); | |

| ➢ | the sections of the Exchange Act that regulate the solicitation of proxies, consents or authorizations in respect of any securities registered under the Exchange Act; | |

| ➢ | the sections of the Exchange Act that require insiders to file public reports of their stock ownership and trading activities and that impose liability on insiders who profit from trades made in a short period of time; and | |

| ➢ | the rules under the Exchange Act that require the filing with the SEC of quarterly reports on Form 10-Q, containing unaudited financial and other specified information, and current reports on Form 8-K, upon the occurrence of specified significant events. |

| S-8 |

We file with the SEC, within four months after the end of each fiscal year (or as otherwise required by the SEC), a prospectus on Form 20-F containing financial statements audited by an independent registered public accounting firm.

We may take advantage of these exemptions until such time as we are no longer a foreign private issuer. We would cease to be a foreign private issuer at such time as more than 50% of our outstanding voting securities are held of record by U.S. residents and any of the following three circumstances applies: (i) the majority of our executive officers or directors are U.S. citizens or residents, (ii) more than 50% of our assets are located in the United States or (iii) our business is administered principally in the United States. Both foreign private issuers and emerging growth companies are also exempt from certain of the more extensive SEC executive compensation disclosure rules. Therefore, if we no longer qualify as an emerging growth company but remain a foreign private issuer, we will continue to be exempt from such rules and will continue to be permitted to follow our home country practice as to the disclosure of such matters.

Corporate Information

Our principal executive offices are located at 8 Amoy Street, #01-01, Singapore 049950, which is also our registered address, and our telephone number is +65 8940 1200. The address of our website is www.geniusgroup.net. Information contained on, or available through, our website does not constitute part of, and is not deemed incorporated by reference into, this prospectus. Our agent for service of process in the United States is Puglisi & Associates, located at 850 Library Avenue, Suite 204, Newark, Delaware 19711.

The Offering

| Series 1 units offered by us in this offering | Up to 15,673,981 Series 1 units. | |

| Series 2 units offered by us in this offering | Up to 15,673,981 Series 2 units. We are offering to those purchasers whose purchase of Series 1 units in this offering would otherwise result in the purchaser, together with its affiliates and certain related parties, beneficially owning more than 4.99% or 9.99%, at the election of the purchaser, of our outstanding ordinary shares following the consummation of this offering, the opportunity to purchase, if such purchaser so chooses, Series 2 units, in lieu of Series 1 units that would otherwise result in beneficial ownership in excess of 4.99% (or, at the election of the purchaser, 9.99%) of our outstanding ordinary shares. | |

| Ordinary shares offered by us in this offering | 15,673,981 ordinary shares (assuming the sale of all units covered by this prospectus, the exercise in full of all pre-funded Series 2024 -B warrants included in the Series 2 units, and no exercise of any Series 2024 -A warrants or Series 2024-C warrants included in the Series 1 or Series 2 units). | |

| Series 2024-A and Series 2024-C warrants offered by us in the offering | Series 2024-A warrants to purchase up to 15,673,981 ordinary shares and Series 2024-C warrants to purchase up to 15,673,981 ordinary shares. Each full Series 2024 -A warrant and each full Series 2024-C warrant will entitle the holder to purchase one ordinary share. The Series 2024 -A warrants and Series 2024-C warrants will be exercisable commencing on the date of issuance and will expire on the five-year anniversary of the date of issuance (for the Series 2024-A warrants) and on the 18 month anniversary of the date of issuance (for the Series 2024-C warrants), for both series of warrants at an assumed exercise price of $0.7018 per share.

This prospectus also relates to the offering of the shares issuable upon exercise of the Series 2024 -A warrants and the Series 2024-C warrants. The exercise price of the Series 2024 -A warrants and Series 2024-C warrants and the number of shares into which the Series 2024 -A warrants and the Series 2024-C warrants may be exercised are subject to adjustment in certain circumstances. | |

| Pre-funded Series 2024 -B warrants offered by us in the offering | Pre-funded Series 2024 -B warrants to purchase up to 15,673,981 shares. Each full pre-funded Series 2024-B warrant, if any, will entitle the holder to purchase one share. The pre-funded Series 2024 -B warrants will be exercisable commencing on the date of issuance and will expire on the five-year anniversary of the date of issuance, at an exercise price of $0.0001 per share. The assumed purchase price of $0.7018 per share will be pre-paid, except for a nominal exercise price of $0.0001 per share, upon issuance of the pre-funded Series 2024 -B warrants and, consequently, no additional payment or other consideration (other than the nominal exercise price of $0.0001 per share) will be required to be delivered to us by the holder upon exercise.

This prospectus also relates to the offering of the ordinary shares issuable upon exercise of the pre-funded Series 2024 -B warrants. The exercise price of the pre-funded Series 2024 -B warrants and the number of shares into which the pre-funded Series 2024 -B warrants may be exercised are subject to adjustment in certain circumstances. |

| S-9 |

| Beneficial Ownership Limitation in Series 2024 -A warrants and Series 2024-C warrants and the pre-funded Series 2024-B warrants | A holder (together with its affiliates) may not exercise any portion of the Series 2024 -A warrants and/or Series 2024-C warrants and/or pre-funded Series 2024 -B warrants to the extent that the holder, together with its affiliates and certain related parties, would beneficially own more than 4.99% (or, at the election of the holder prior to the date of issuance, 9.99%) of our outstanding ordinary shares after exercise. The holder may increase or decrease this beneficial ownership limitation to any other percentage not in excess of 9.99% upon notice to us, provided that, in the case of an increase of such beneficial ownership limitation, such notice shall not be effective until 61 days following notice to us. | |

| Shares outstanding after this offering | 84,648,280 ordinary shares (assuming the exercise of all of the pre-funded Series 2024 -B warrants). | |

| Use of proceeds | We estimate that our net proceeds from this offering will be approximately $9,950,000, assuming no exercise of any Series 2024 -A warrants or Series 2024-C warrants issued in this offering, after deducting the placement agent’s fees and estimated offering expenses payable by us.

We intend to use the net proceeds received from this offering to fund working capital and for other general corporate purposes. See “Use of Proceeds.”

Because this is a best efforts offering with no minimum amount of securities or offering proceeds as a condition to closing, we may not sell all or any of the securities offered hereby. As a result, we may receive significantly less in net proceeds than we currently estimate. | |

| Risk factors | Investing in our securities involves a high degree of risk. See the section entitled “Risk Factors” of this prospectus and the section entitled “Risk Factors” in the documents incorporated by reference herein for a discussion of factors you should carefully consider before investing in our securities. | |

| NYSE American symbol | “GNS.” The Series 2024 -A warrants, the Series 2024-C warrants and the pre-funded Series 2024 -B warrants are not, and will not be, listed for trading on any national securities exchange or other nationally recognized trading system, including the NYSE American. |

Unless otherwise noted, the number of ordinary shares to be outstanding immediately after this offering as set forth above is based on 73,873,784 shares outstanding as of December 27, 2023, and excludes:

| ● | 2,516,581 management and employee share options issued and reserved. | |

| ● | Any further conversion from the convertible debt issuance or any outstanding warrants. |

Unless otherwise indicated, the information in this prospectus assumes no exercise of the Series 2024 -A warrants or Series 2024-C warrants or the Placement Agent Warrants (as hereinafter defined) offered hereby.

| S-10 |

SUMMARY COMBINED UNAUDITED PRO FORMA FINANCIAL DATA AND CONSOLIDATED FINANCIAL DATA

Please refer to the glossary of terms provided in the Prospectus Summary for aid in understanding the entities, acquisitions, products, services and certain other concepts referred to in the financial data presented herein.

The following tables set forth summarizes combined pro forma financial data and summary consolidated financial data for the periods and as of the dates indicated. The summary combined unaudited pro forma financial data below includes the consolidated financials of all companies in the Genius Group, including the Pre-IPO Group and the Acquisitions as if they were operating as one group in the periods indicated and excludes the spin-off entity, Entrepreneur Resorts Ltd. The pro forma financials for period ended June 30, 2023 include the financial data of the Pre-IPO Group and Acquisitions from the audited financials and the unaudited financial data of the Acquisitions.

The summary income data for the years ended December 31, 2022 and the interim periods ended June 30, 2023 and 2022 and the summary balance sheet data as of June 30, 2023 and December 31, 2022 for the Group are derived from the consolidated financial statements included in the Company’s Amended Annual Report. Our consolidated financial statements have been prepared in U.S. dollars and in accordance with IFRS, as issued by the IASB

On January 30, 2023, the Board of Directors for Genius Group Ltd, approved with conditions of Singapore court approval, the spinoff of Entrepreneur Resorts Ltd. This spinoff was completed in order to further its strategy for streamlining and rationalize the group’s operations into Genius with its Edtech focus, and ERL, with its hospitality focus. On August 1, 2023, the Singapore court approved the group to spinoff of ERL from the group which enabled the management teams of both companies to grow their respective business models most effectively. The Company also announced the record date on August 31, 2023 with the spin-off completed on October 2, 2023.

Genius Group is made up of nine companies (taking into account the Acquisitions) that have varying financial performance. For this reason, you should read the summary combined pro forma financial data in conjunction with our audited consolidated financial statements and related notes beginning on page F-1 of the Company’s Prospectus, and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included elsewhere in the Company’s Prospectus. Our historical results do not necessarily indicate our expected results for any future periods.

Financial Statement Data

| Group Unaudited Financials Six months Ended June 30, | Group Audited Financials Year Ended December 31, | |||||||||||||||

| 2023 | 2022 | 2022 | 2021 | |||||||||||||

| (USD 000’s) | (USD 000’s) (Restated) | (USD 000’s) | (USD 000’s) | |||||||||||||

| Sales | 11,796 | 5,343 | 18,194 | 8,295 | ||||||||||||

| Cost of goods sold | (5,593 | ) | (3,112 | ) | (9,555 | ) | (5,537 | ) | ||||||||

| Gross profit | 6,203 | 2,231 | 8,639 | 2,757 | ||||||||||||

| Other Operating Income | 4 | 225 | 280 | 324 | ||||||||||||

| Operating Expenses | (15,369 | ) | (5,428 | ) | (50,502 | ) | (7,250 | ) | ||||||||

| Operating Loss | (9,162 | ) | (2,972 | ) | (41,583 | ) | (4,168 | ) | ||||||||

| Other income | 68 | 31 | 419 | 0 | ||||||||||||

| Other Expense | (2,005 | ) | (580 | ) | (15,151 | ) | (450 | ) | ||||||||

| Net Loss Before Tax | (11,099 | ) | (3,521 | ) | (56,315 | ) | (4,618 | ) | ||||||||

| Tax Benefits | 325 | 24 | 1,064 | 129 | ||||||||||||

| Net Loss After Tax | (10,774 | ) | (3,497 | ) | (55,252 | ) | (4,489 | ) | ||||||||

| Other Comprehensive Loss | (600 | ) | (70 | ) | (1,045 | ) | 230 | |||||||||

| Total Loss | (11,374 | ) | (3,567 | ) | (56,297 | ) | (4,259 | ) | ||||||||

| Net income per share, basic and diluted | (0.32 | ) | (0.20 | ) | (2.44 | ) | (0.28 | ) | ||||||||

| Weighted-average number of shares outstanding, basic and diluted | 33,668,483 | 17,794,634 | 22,634,366 | 16,155,812 | ||||||||||||

| S-11 |

Group Unaudited Financials Six months ended June 30 | Group Audited Financials year ended December 31,

| |||||||||||

| 2023 | 2022 | 2021 | ||||||||||

| (USD 000’s) | (USD 000’s) | (USD 000’s) | ||||||||||

| Summary Balance Sheet Data: | ||||||||||||

| Total current assets | 9,350 | 24,251 | 6,496 | |||||||||

| Total non-current assets | 66,052 | 67,009 | 11,099 | |||||||||

| Total Assets | 75,402 | 91,260 | 17,595 | |||||||||

| Total current liabilities | 17,486 | 23,378 | 7,140 | |||||||||

| Total non-current liabilities | 51,776 | 53,927 | 2,469 | |||||||||

| Total Liabilities | 69,262 | 77,305 | 9,609 | |||||||||

| Total Stockholders’ Equity | 6,140 | 13,955 | 7,986 | |||||||||

| Total Liabilities and Shareholders’ Equity | 75,402 | 91,260 | 17,595 | |||||||||

Pro forma Financials

Pro forma financials are derived by reducing the financial impact of spin off of Entrepreneur Resorts Ltd and adding back acquisition financials for the period prior to acquisition date. Due to the intercompany receivable from Entrepreneur Resorts Ltd, the balance sheet effect of spin-off results in an increase in assets (current assets) which is reflected by a negative balance under Entrepreneur Resorts Ltd.

Genius Group Unaudited Pro forma Six Months Ended June 30, 2023 | ||||||||||||||||

| Unaudited Financials | Entrepreneur Resorts | Acquisitions | Pro forma Financials | |||||||||||||

| (USD 000’s) | (USD 000’s) | (USD 000’s) | (USD 000’s) | |||||||||||||

| Sales | 11,796 | (2,834 | ) | - | 8,962 | |||||||||||

| Cost of goods sold | (5,594 | ) | 963 | - | (4,631 | ) | ||||||||||

| Gross profit | 6,202 | (1,871 | ) | - | 4,331 | |||||||||||

| Other Operating Income | 4 | 3 | - | 7 | ||||||||||||

| Operating Expenses | (15,369 | ) | 1,613 | - | (13,756 | ) | ||||||||||

| Operating Loss from the continuing operations | (9,163 | ) | (255 | ) | - | (9,418 | ) | |||||||||

Genius Group Unaudited Pro forma Year Ended December 31, 2022 | ||||||||||||||||

| Audited Financials | Entrepreneur Resorts | Acquisitions | Pro forma Financials | |||||||||||||

| (USD 000’s) | (USD 000’s) | (USD 000’s) | (USD 000’s) | |||||||||||||

| Sales | 18,194 | (4,660 | ) | 9,936 | 23,470 | |||||||||||

| Cost of goods sold | (9,555 | ) | 2,776 | (3,773 | ) | (10,552 | ) | |||||||||

| Gross profit | 8,639 | (1,884 | ) | 6,162 | 12,918 | |||||||||||

| Other Operating Income | 280 | (95 | ) | - | 185 | |||||||||||

| Operating Expenses | (50,502 | ) | 11,725 | (6,512 | ) | (45,289 | ) | |||||||||

| Operating Loss from the continuing operations | (41,583 | ) | 9,746 | (349 | ) | (32,186 | ) | |||||||||

Genius Group Unaudited Pro forma Six months Ended June 30, 2023 | ||||||||||||||||

| Unaudited Financials | Entrepreneur Resorts | Pro forma Adjustment | Pro forma Financials | |||||||||||||

| (USD 000’s) | (USD 000’s) | (USD 000’s) | (USD 000’s) | |||||||||||||

| Summary Balance Sheet Data: | ||||||||||||||||

| Total current assets | 9,350 | 3,229 | - | 12,579 | ||||||||||||

| Total non-current assets | 66,052 | (946 | ) | - | 65,106 | |||||||||||

| Total Assets | 75,402 | 2,283 | - | 77,685 | ||||||||||||

| Total current liabilities | 17,486 | (2,527 | ) | - | 14,959 | |||||||||||

| Total non-current liabilities | 51,776 | (2,266 | ) | - | 49,511 | |||||||||||

| Total Liabilities | 69,262 | (4,793 | ) | - | 64,470 | |||||||||||

| Total Stockholders’ Equity | 6,140 | 7,076 | - | 13,216 | ||||||||||||

| Total Liabilities and Shareholders’ Equity | 75,402 | 2,283 | - | 77,686 | ||||||||||||

Non-IFRS Financial Measures — Adjusted EBITDA

We have included Adjusted EBITDA in this Prospectus because it is a key measure used by our management and board of directors to understand and evaluate our core operating performance and trends, to prepare and approve our annual budget and to develop short- and long-term operational plans. In particular, the exclusion of certain expenses in calculating Adjusted EBITDA can provide a useful measure for period-to-period comparisons of our core business. Non-IFRS financial measures are not a substitute for IFRS financial measures.

We calculate Adjusted EBITDA as Net loss for the period plus income taxes plus/ minus net finance result plus depreciation and amortization plus/minus share-based compensation expenses plus bad debt provision. Share-based compensation expenses and bad debt provision are included in General and administrative expenses in the Consolidated Statements of Operations.

Derived from Financial Statement Data

Group Unaudited Financials Six months ended June 30, | Group Audited Financials Year ended December 31, | |||||||||||||||

| 2023 | 2022 | 2022 | 2021 | |||||||||||||

| (USD 000’s) | (USD 000’s) (Restated) | (USD 000’s) | (USD 000’s) | |||||||||||||

| Net Loss | (10,775 | ) | (3,497 | ) | (55,252 | ) | (4,489 | ) | ||||||||

| Tax Benefits | (325 | ) | (24 | ) | (1,064 | ) | (129 | ) | ||||||||

| Interest Expense, net | 1,999 | 99 | 1,312 | 450 | ||||||||||||

| Depreciation and Amortization | 1,209 | 836 | 2,351 | 1,575 | ||||||||||||

| Impairment | - | 480 | 28,246 | - | ||||||||||||

| Revaluation Adjustment of Contingent Liabilities | - | - | 13,838 | - | ||||||||||||

| Stock Based Compensation | 403 | 150 | 1,309 | 294 | ||||||||||||

| Bad Debt Provision | 170 | - | 1,509 | (39 | ) | |||||||||||

| Adjusted EBITDA | (7,318 | ) | (1,956 | ) | (7,750 | ) | (2,338 | ) | ||||||||

| S-12 |

Pro forma Financials

Pro forma EBITDA is derived by reducing the financial impact of spin off of Entrepreneur Resorts Ltd and adding back acquisition financials for the period prior to acquisition date.

Genius Group Unaudited Pro forma Six Months Ended June 30, 2023 | ||||||||||||||||

| Unaudited Financials | Entrepreneur Resorts | Acquisitions | Pro forma Financials | |||||||||||||

| (USD 000’s) | (USD 000’s) | (USD 000’s) | (USD 000’s) | |||||||||||||

| Net Loss | (10,775 | ) | - | - | (10,775 | ) | ||||||||||

| Tax Benefits | (325 | ) | - | - | (325 | ) | ||||||||||

| Interest Expense, net | 1,999 | - | - | 1,999 | ||||||||||||

| Depreciation and Amortization | 1,209 | (30 | ) | - | 1,179 | |||||||||||

| Impairment | - | - | - | - | ||||||||||||

| Revaluation Adjustment of Contingent Liabilities | - | - | - | - | ||||||||||||

| Stock Based Compensation | 403 | - | 403 | |||||||||||||

| Bad Debt Provision | 170 | - | 170 | |||||||||||||

| Adjusted EBITDA | (7,318 | ) | (30 | ) | - | (7,348 | ) | |||||||||

Genius Group Unaudited Pro forma Year Ended December 31, 2022 | ||||||||||||||||

| Audited Financials | Entrepreneur Resorts | Acquisitions | Pro forma Financials | |||||||||||||

| (USD 000’s) | (USD 000’s) | (USD 000’s) | (USD 000’s) | |||||||||||||

| Net Loss | (55,252 | ) | - | 348 | (54,903 | ) | ||||||||||

| Tax Benefits | (1,064 | ) | - | - | (1,064 | ) | ||||||||||

| Interest Expense, net | 1,312 | - | 12 | 1,325 | ||||||||||||

| Depreciation and Amortization | 2,351 | (1,105 | ) | 103 | 1,348 | |||||||||||

| Impairment | 28,246 | (7,986 | ) | - | 20,260 | |||||||||||

| Revaluation Adjustment of Contingent Liabilities | 13,838 | - | - | 13,838 | ||||||||||||

| Stock Based Compensation | 1,309 | (111 | ) | - | 1,198 | |||||||||||

| Bad Debt Provision | 1,509 | (9 | ) | 19 | 1,520 | |||||||||||

| Adjusted EBITDA | (7,750 | ) | (9,211 | ) | 482 | (16,479 | ) | |||||||||

Key Business Metrics

Education segment — Genius Group (including Acquisitions)

| Key Business Metrics – Education Segment | ||||||||||||

| For the six months ended June 30, 2023 | For the year

ended December 31,2022 | For the year

ended December 31,2021 | ||||||||||

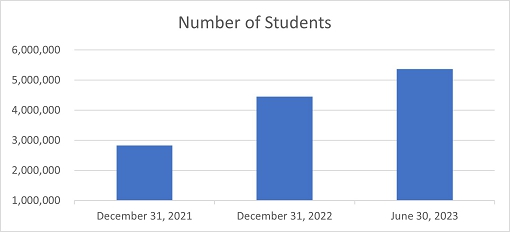

| Number of students and users | 5,365,626 | 4,450,852 | 2,825,628 | |||||||||

| Number of Free Students and users | 5,186,477 | 4,278,933 | 2,768,530 | |||||||||

| Number of Paying Students and users | 179,149 | 171,919 | 72,422 | |||||||||

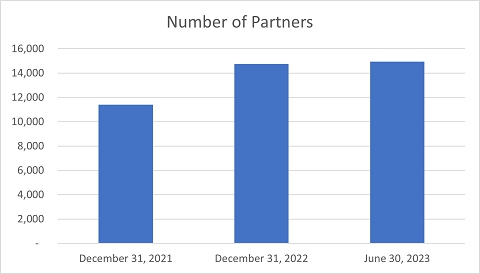

| Number of Partners | 14,942 | 14,760 | 11,414 | |||||||||

| Number of countries of operation | 191 | 191 | 191 | |||||||||

| Marketing Spend | 849,155 | 1,994,331 | 1,139,928 | |||||||||

| Education Revenue | 8,961,780 | 23,469,609 | 25,468,253 | |||||||||

| Revenue from New Paying Students | 2,796,560 | 10,164,848 | 7,377,236 | |||||||||

| New Students | 450,741 | 1,640,698 | 890,328 | |||||||||

| New Paying Students | 8,488 | 19,681 | 10,425 | |||||||||

| Conversion rate | 1.88 | % | 1.20 | % | 1.17 | % | ||||||

| Average Acquisition Cost per New Paying Student | 100 | 101 | 109 | |||||||||

| Average Annual Revenue per New Paying Student | 329 | 516 | 707 | |||||||||

| Net Income (Loss) margin | (48.48 | )% | (172.07 | )% | (4.56 | )% | ||||||

| Adjusted EBITDA margin | (29.00 | )% | (11.76 | )% | 4.10 | % | ||||||

The key business metrics for education segment is measured and calculated as

Number of students and users – The Number of Students, Number of Free Students, and Number of Paying Students are the total numbers for each at the end of the year. For purposes of determining the Number of Students, we treat each student account that registers with a unique email as a student and adjust for any cancellations. This number is then divided into the Number of Paying Students, who have made one or more purchases, and the Number of Free Students, who are utilizing our free courses and products without making a purchase.

Number of Partners - The Number of Partners is the total number of partners at the end of the year. For purposes of determining our Number of Partners, we treat each partner account who registers as a partner with an ability to earn on our platform as a partner.

Number of countries of operation – The Number of Countries of Operation is the total number of countries in which we have students or partners at the end of the year.

Marketing Spend - The Marketing Spend is the total annual marketing spend by the business to acquire new students and partners.

Education Revenue - Education Revenue is all revenue from the education segment of our total revenue.

Revenue from New Paying Students - Revenue from New Paying Students is the total amount of revenue generated from new paying students for the year.

New Students and New Paying Students - New Students is the total number of new students who joined as a student during the period. New Paying Students is the total number of paying students who have become customers for the first time during the year.

Conversion Rate - Conversion rate is calculated as the total students (including free students and paying students) converting into paying students and is derived by dividing the number of new paying students by the total number of new students.

Average Acquisition Cost per New Paying Student – The Average Acquisition Cost per New Paying Student is calculated by dividing the Marketing Spend by the Number of New Paying Students.

Average Annual Revenue per New Paying Student – This metric is calculated as the total revenue for the year derived from New Paying Students divided by the total number of New Paying Students.

Net Income (Loss) margin – The net income (Loss) margin is calculated as net income divided by the total education revenue.

Adjusted EBITDA margin – The adjusted EBITDA margin is calculated as Adjusted EBITDA divided by the total education revenue. The Adjusted EBITDA is Net Income (Loss) excluding tax expenses, interest expenses, depreciation and amortization, impairment, Revaluation Adjustment of Contingent Liabilities, stock-based compensation and bad debt provision.

| S-13 |

Campus segment – Entrepreneur Resorts (spin-off completed on October 2, 2023)

| Key Business Metrics – Campus Segment | ||||||||||||

| For the six months

ended June 30, 2023 | For the year

ended December 31, 2022 | For the year

ended December 31, 2021 | ||||||||||

| Revenue | 2,833,933 | 4,638,122 | 3,100,750 | |||||||||

| No of Locations | 6 | 6 | 6 | |||||||||

| No of Seats/Rooms | 367 | 367 | 367 | |||||||||

| Utilization | 35 | % | 33 | % | 28 | % | ||||||

| Total Orders | 70,454 | 136,204 | 96,390 | |||||||||

| Revenue Per Order | 40 | 34 | 32 | |||||||||

The key business metrics for campus segment is measured and calculated as

Note on Campus segment business models

Our campus segment is divided into our three venue models within Entrepreneur Resorts, described as follows

Cafe — Our Cafe model is our smaller scale venue combining a cafe, co-working space, education and event space, with revenue from food & beverage, home delivery and venue rental.

Central — Our Central model is our larger scale venue combining a cafe, co-working space, education and event space, with revenue from food & beverage, home delivery and venue rental.

Resort — Our Resort model is our resort campus with revenue from accommodation, food and beverage, spa and ancillary services and conference facilities.

Revenue - Revenue is all revenue from the campus segment of our total revenue.

No of Locations – Location is the total operating location within campus segment.

No of Seats/Rooms - For Cafe and Central locations, this is a measure of the number of customer seats on premises at the end of the year. For Resort locations, this is a measure of the daily number of available guest rooms at the end of the year.

Utilization - Utilization is the percentage of the total capacity of Seats and Rooms that is utilized in orders throughout the year.

Total Order - This metric is calculated as the total number of customer orders fulfilled by each of our venues during the year. The number includes dine-in, take away and delivery orders.

Revenue Per Order - This metric is calculated as Revenue divided by Total Orders.

RISK FACTORS

Investing in our ordinary shares is highly speculative and involves a significant degree of risk. You should carefully consider the following risks, as well as other information contained in this prospectus, before making an investment in our Company. The risks discussed below could materially and adversely affect our business, prospects, financial condition, results of operations, cash flows, ability to pay dividends and the trading price of our ordinary shares. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial may also materially and adversely affect our business, prospects, financial condition, results of operations, cash flows and ability to pay dividends, and you may lose all or part of your investment.

Risks Related to Our Business and Industry (All Group Companies)

Investing in our ordinary shares is highly speculative and involves a significant degree of risk. You should carefully consider the following risks, as well as other information contained in this Prospectus, before making an investment in our Company. The risks discussed below could materially and adversely affect our business, prospects, financial condition, results of operations, cash flows, ability to pay dividends and the trading price of our ordinary shares. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial may also materially and adversely affect our business, prospects, financial condition, results of operations, cash flows and ability to pay dividends, and you may lose all or part of your investment.

| S-14 |

Going Concern

Pursuant to IAS 1, Presentation of Financial Statements, the Company is required to and does evaluate at each annual and interim period whether there are conditions or events, considered in the aggregate, that raise substantial doubt about its ability to continue as a going concern within one year after the date that the consolidated financial statements are issued. Based on the definitions in the relevant accounting standards, and due to recent changes in the Company’s 2022 convertible loan terms in which company elected to pay all future payments in cash, negative cash flows, and continued net losses, management has determined that without additional capital raised, in the next twelve months, there is substantial doubt about the Company’s ability to continue as a going concern. This has been disclosed in the audit report of the Company’s amended audit report published in the form of 20-F/A.

The Company’s consolidated financial statements as of June 30, 2023 and December 31,2022 have been prepared on a going concern basis. Although the Company has taken, and plans to continue to take, proactive measures to enhance its liquidity position and provide additional financial flexibility, including discussions with lenders and bankers, there can be no assurance that these measures, including the timing and terms thereof, will be successful or sufficient.

The substantial doubt about the Company’s ability to continue as a going concern may negatively affect the price of the Company’s ordinary shares, may impact relationships with third parties with whom the Company does business, including customers, vendors and lenders, may impact the Company’s ability to raise additional capital or implement its business plan.

Risks Related to Our Business and Industry (All Group Companies)

We are a global business subject to complex economic, legal, political, tax, foreign currency and other risks associated with international operations, which risks may be difficult to adequately address.

In 2021, 2022 and first half of 2023, over 90% of our revenues from the Pre-IPO Group were generated from operations outside of the United States. When including the Acquisitions, over 50% of our pro forma revenues for Genius Group for these same periods were generated from operations outside of the United States. Our GeniusU Edtech platform has students in 191 countries, each of which is subject to complex business, economic, legal, political, tax and foreign currency risks. As we continue to expand our international operations with our Acquisitions, we may have difficulty managing and administering a globally dispersed business and we may need to expend additional funds to, among other things, staff key management positions, obtain additional information technology infrastructure and successfully implement relevant course and program offerings for a significant number of international markets, which may materially adversely affect our business, financial condition and results of operations.

Additional challenges associated with the conduct of our business overseas that may materially adversely affect our operating results include:

| ➢ | the large scale and diversity of our operational institutions present numerous challenges, including difficulty in staffing and managing foreign operations as a result of distance, language, legal, labor relations and other differences; | |

| ➢ | each of our programs and services are subject to unique business risks and challenges including competitive pressures and diverse pricing environments at the local level; | |

| ➢ | difficulty maintaining quality standards consistent with our brands and with local accreditation requirements; | |

| ➢ | fluctuations in exchange rates, possible currency devaluations and currency controls, inflation and hyperinflation; | |

| ➢ | difficulty selecting and monitoring partners in different jurisdictions; | |

| ➢ | compliance with a wide variety of domestic and foreign laws and regulations; | |

| ➢ | expropriation of assets by governments; | |

| ➢ | political elections and changes in government policies; | |

| ➢ | changes in tax laws, assessments or enforcement by taxing authorities in different jurisdictions; | |

| ➢ | difficulty protecting our intellectual property rights overseas due to, among other reasons, the uncertainty of laws and enforcement in certain countries relating to the protection of intellectual property rights; | |

| ➢ | lower levels of availability or use of the Internet, through which our online programs are delivered; |

| ➢ | limitations on the repatriation and investment of funds, foreign currency exchange restrictions and inability to transfer cash back to the United States without taxation; | |

| ➢ | potential economic and political instability the countries in which we operate, including student unrest; or | |

| ➢ | business interruptions from acts of terrorism, civil disorder, labor stoppages, public health risks, crime and natural disasters, particularly in areas in which we have significant operations. |

| S-15 |

Our success in growing our business profitably will depend, in part, on the ability to anticipate and effectively manage these and other risks related to operating in various countries. Any failure by us to effectively manage the challenges associated with the maintenance or expansion of our international operations could materially adversely affect our business, financial condition and results of operations.

Our growth strategy anticipates that we will create new products, services, and distribution channels and expand existing distribution channels. If we are unable to effectively manage these initiatives, our business, financial condition, results of operations and cash flows would be adversely affected.

As we create new products, services, and distribution channels and expand our existing distribution channels, we expect to face challenges distinct from those we currently encounter, including:

| ➢ | The challenge of tailoring new products and services to new technologies as they develop, including artificial intelligence, augmented reality and virtual reality; | |

| ➢ | Additional local competition as we localize our products and services to different countries, cultures and languages, each with new, local distribution channels; | |